Cement Sector Q1 FY26 Highlights: UltraTech Cement Leads, Shree Cement Surges, Ambuja Cement Strengthens

Introduction

India’s cement sector kicked off FY26 on a strong note as UltraTech Cement, Shree Cement, and Ambuja Cements posted robust quarterly results amid a broader rebound across the industry. Fueled by government infrastructure impetus, improved pricing, and rising demand, the cement market appears to be cementing its growth trajectory for the year ahead. This article takes a closer look at each giant's Q1 performance and positions them against the macro backdrop of the sector.

Indian Cement Industry Overview – 2025

Positioned right after China, India’s cement industry has developed a formidable installed capacity of nearly 570 MTPA, with FY25 output expected to be around 430 million tonnes. The industry accounts for nearly 7% of global supply, underscoring its importance in both housing and infrastructure development. Expansion is being fuelled by government-backed initiatives such as affordable housing under PMAY, metro rail networks, expressways, and transformative mega projects like the Mumbai–Ahmedabad Bullet Train corridor.

Cement demand is expected to grow by 7–8% in FY25, supported by both urban real estate and rural housing, with industry size projected to reach 600 million tonnes by 2030 at a CAGR of 5–6%. Exports remain strong at Rs. 5,500 crore in FY24, while imports are negligible due to abundant limestone reserves.

Cement majors like UltraTech, Adani Cement, Shree Cement, Dalmia Bharat, and ACC-Ambuja are investing in growth by setting up new facilities and expanding existing ones. Sustainability is also a key focus, with increased use of green cement, renewable energy, and digital technologies.

Overall, the industry in 2025 stands at a critical growth stage, balancing rising demand, cost pressures, and sustainability commitments.

Company Overview

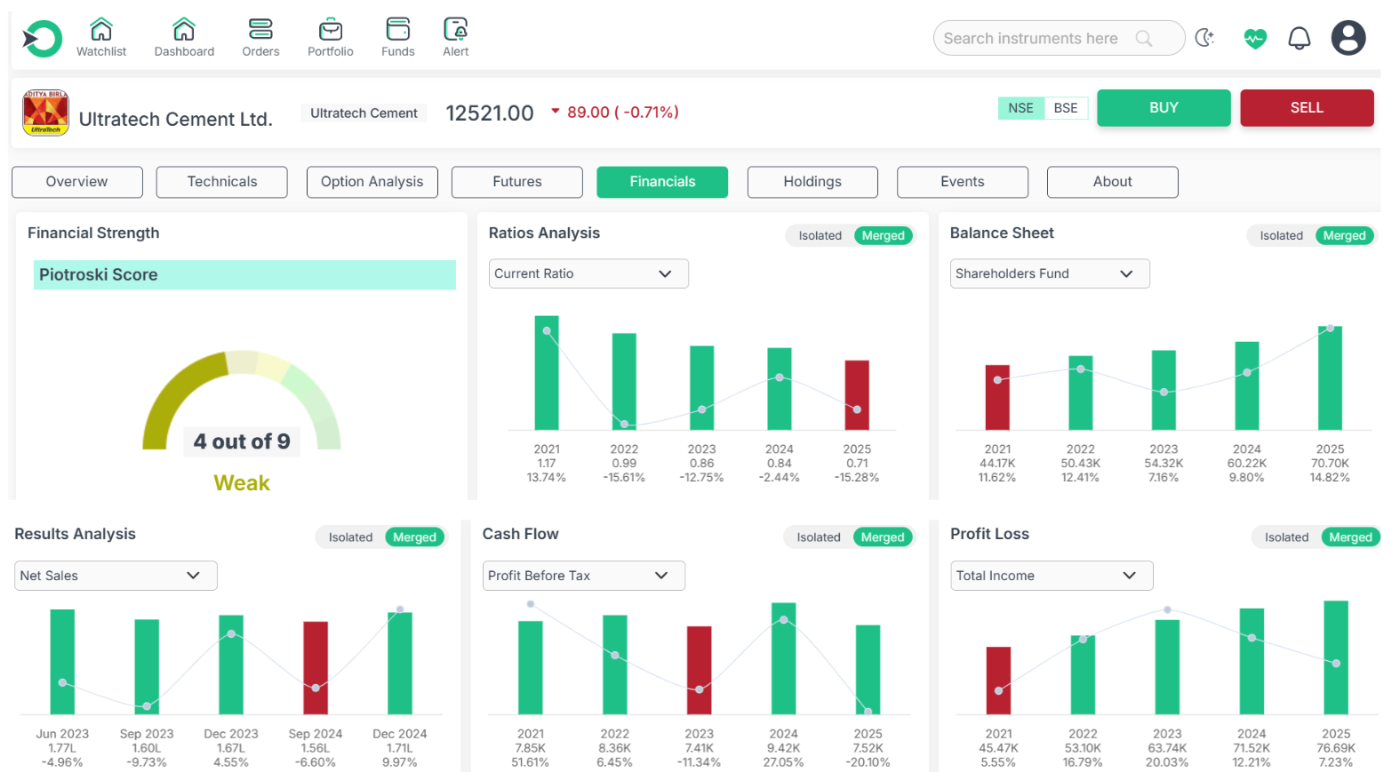

UltraTech Cement Limited

UltraTech Cement Limited, the flagship enterprise of the Aditya Birla Group, stands as India’s largest cement manufacturer and is also among the top three players globally beyond China. Its consolidated grey cement capacity of 192.26 MTPA is supported by an extensive network of 34 integrated plants, 34 grinding units, and close to 395 ready-mix concrete facilities nationwide, while its presence also stretches internationally to the UAE, Bahrain, and Sri Lanka.

UltraTech is also a leader in sustainable practices, being a signatory to the GCCA Climate Ambition 2050 and committed to achieving net-zero concrete. With innovative solutions like UltraTech Building Solutions (UBS) and a strong focus on green cement, the company continues to set benchmarks in scale, innovation, and sustainability.

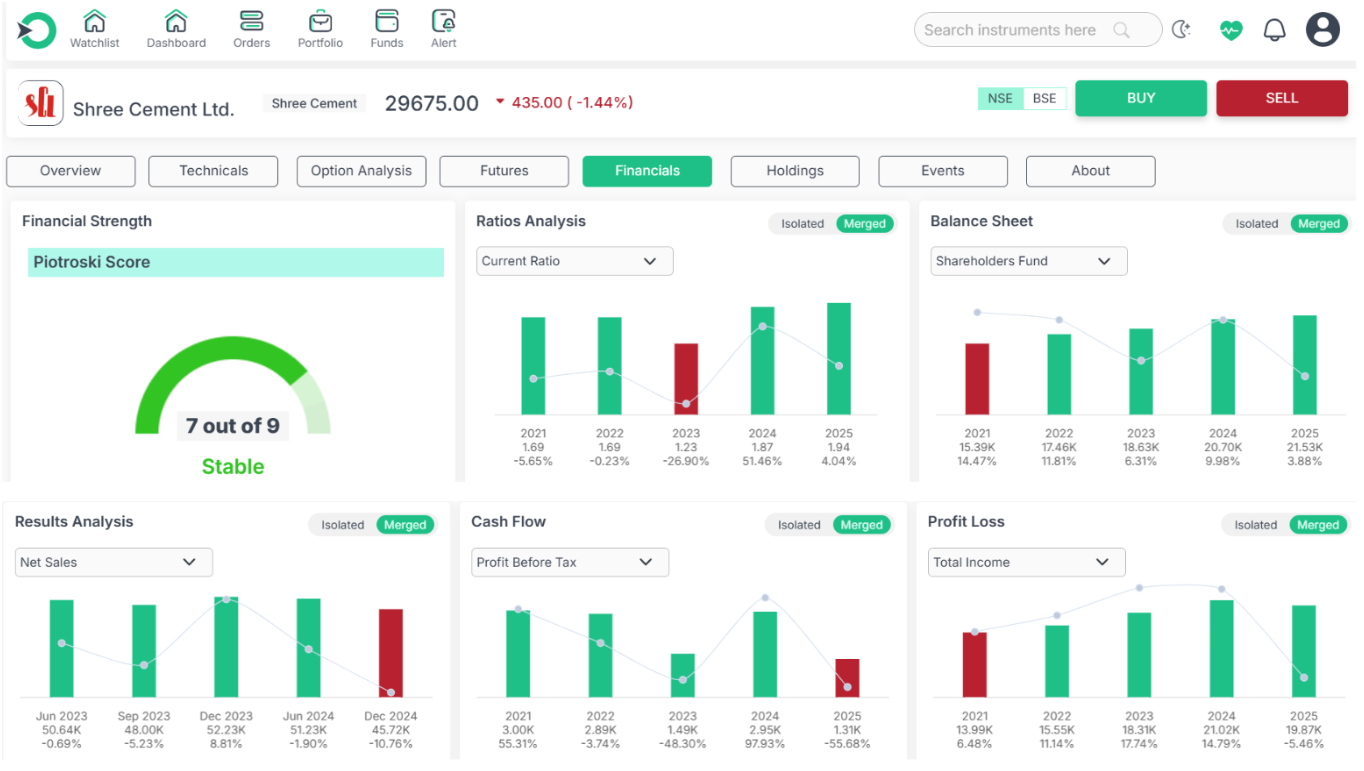

Shree Cement Limited

Shree Cement Limited is among India’s leading cement manufacturers, recognized for efficiency, sustainability, and stakeholder-centric growth. Guided by the Rigveda mantra “Let noble thoughts come to us from all over the world”, it focuses on transparency, integrity, and sustainable practices. With a culture built on care, innovation, trust, and efficiency, the company strives to deliver value to investors, employees, customers, communities, and the environment.

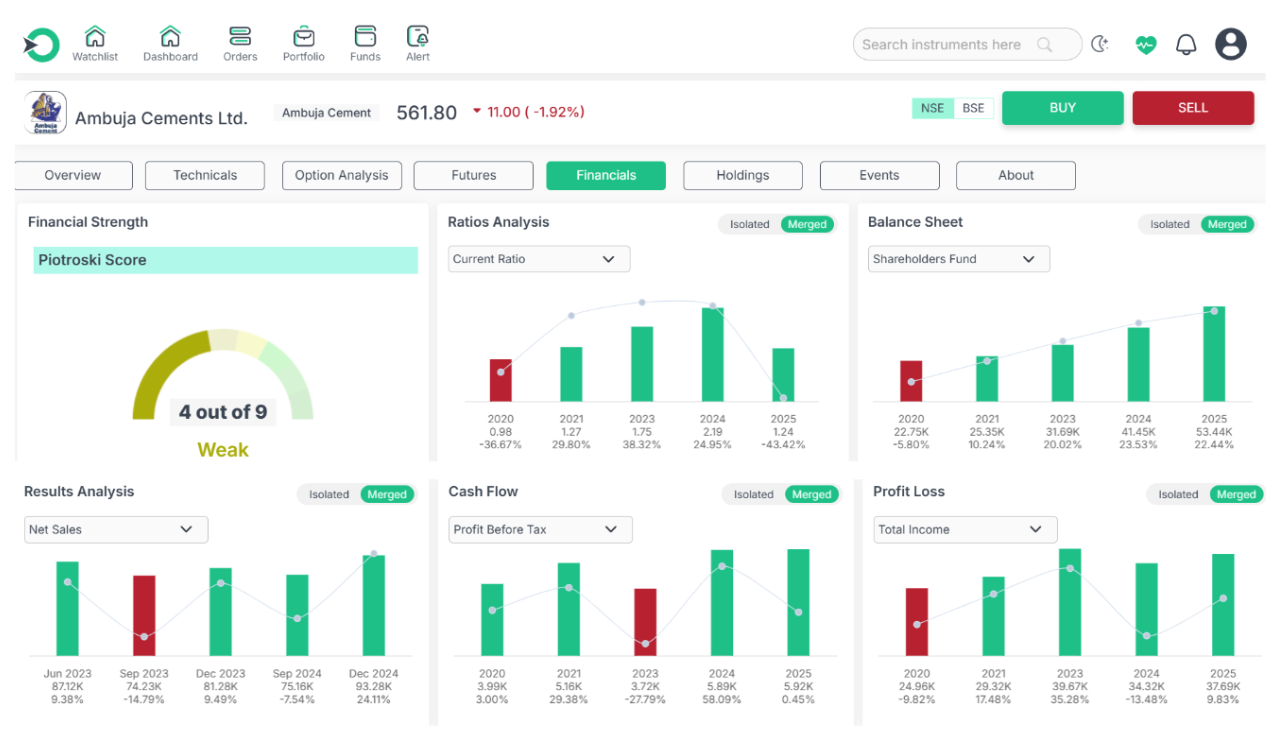

Ambuja Cements Limited

Ambuja Cements Limited, a key subsidiary of the Adani Group, stands among India’s foremost cement manufacturers.With a current capacity of 76 MTPA, the company has set an ambitious target of reaching 140 MTPA by 2028 through strategic acquisitions including Sanghi, Penna, and Orient Cement. Known for its strong distribution network and customer-centric approach, Ambuja plays a key role in supporting India’s infrastructure growth. Backed by Adani’s vision, the company emphasizes operational efficiency, sustainability, and innovation to strengthen its position as a major player in the cement industry.

Q1 FY26 Results: UltraTech Cement, Shree Cement, and Ambuja Cement

The Q1 FY26 results of UltraTech Cement, Shree Cement, and Ambuja Cement highlight how India’s leading cement players navigated demand trends, cost pressures, and profitability challenges.

|

Field (Rs. in Cr) |

UltraTech Cement Ltd. |

Shree Cement Ltd. |

Ambuja Cements Ltd. |

|

Total Revenue / Income |

21,275.45 |

5,280.88 |

10,289.07 |

|

Cost of Revenue |

8,680.94 |

1,747.64 |

1,524.46 |

|

Gross Profit |

12,594.51 |

3,533.24 |

8,719.65 |

|

Total Operating Expense |

16,865.11 |

3,948.28 |

8,327.98 |

|

Selling & Administrative Expenses |

5,621.21 |

1,465.47 |

2,422.53 |

|

Other Operating Expenses |

11,243.90 |

1,318.91 |

5,905.45 |

|

Selling & Marketing Exp. |

0 |

1,163.90 |

0 |

|

Depreciation & Amortization |

1,106.78 |

653.81 |

861.57 |

|

Operating Profit |

4,410.34 |

1,332.60 |

1,961.09 |

|

Interest Income |

437.61 |

45.53 |

62.98 |

|

Other Income (Net) |

0 |

189.7 |

0 |

|

EBITDA |

4,552.87 |

1,566.83 |

2,079.56 |

|

EBIT |

3,446.09 |

913.02 |

1,217.99 |

|

Interest Expense |

433.3 |

45.53 |

67.14 |

|

Profit Before Tax |

3,012.11 |

868.49 |

1,328.47 |

|

Income Tax Expense |

786.89 |

224.83 |

362.97 |

|

Net Profit |

2,225.90 |

642.66 |

787.88 |

|

EPS (Rs. ) |

75.54 |

178.12 |

3.2 |

Revenue Performance

UltraTech Cement posted the highest revenue among the three players, reporting Rs. 21,275 crore in Q1 FY26, a growth of 13% YoY, supported by stronger sales volumes and contributions from recent acquisitions. Ambuja Cements followed with Rs. 10,289 crore, registering an impressive 23% YoY increase, marking its best-ever quarterly revenue, backed by rising demand and successful integration of Orient Cement assets. Shree Cement, though smaller in scale, reported Rs. 4,948 crore, reflecting a modest 2% YoY growth, largely driven by its core operations and premium product portfolio.

This indicates UltraTech’s dominance in size, while Ambuja showed the sharpest revenue growth momentum, and Shree maintained stability.

Profitability (Net Profit)

UltraTech Cement delivered the highest net profit at Rs. 2,225.9 crore, a 49% YoY rise underscoring its scale and operational efficiencies. Ambuja Cements followed with Rs. 787.9 crore, up 24% YoY, reflecting margin gains and disciplined cost management. Shree Cement, though smaller in absolute terms, impressed with Rs. 619 crore, marking a stellar 95% YoY growth on the back of efficiency gains and an improved product mix. Overall, UltraTech dominated in sheer profit size, Shree shone in growth momentum, and Ambuja sustained healthy progress.

EBITDA & Margins

UltraTech Cement recorded Rs. 4,552.9 crore EBITDA, an increase of 44% YoY, with margins improving to 21.4%. Ambuja Cements reported Rs. 1,961 crore EBITDA, up 53% YoY, with margins of 19.1%, reflecting efficiency gains and cost savings. Shree Cement posted Rs. 1,229 crore EBITDA, achieving 34% YoY growth with margins at around 24.8%, among the strongest in the sector.

All three showed significant EBITDA improvement, with Shree excelling in margin strength, Ambuja in growth momentum, and UltraTech in absolute value.

Operating Efficiency & Costs

Ambuja’s operating expenses stood at Rs. 8,328 crore, well-managed relative to revenue growth, supporting strong profitability. UltraTech, due to its massive scale, incurred higher operating expenses of Rs. 16,865 crore, though cost-saving initiatives such as a 12% YoY reduction in energy costs cushioned pressure. Shree Cement’s operating expenses were Rs. 3,948 crore, reflecting disciplined cost control, with lower energy costs in UAE operations significantly boosting profitability.

Ambuja stood out in balancing growth with controlled costs, while UltraTech demonstrated efficiency at scale, and Shree showcased sharp improvements from cost discipline.

Earnings per Share (EPS)

EPS remained a differentiating factor across companies. Shree Cement delivered the highest EPS at Rs. 178.1, reflecting its ability to generate higher shareholder returns despite smaller revenue size. UltraTech posted Rs. 75.5 per share, benefiting from strong profitability and scale. Ambuja, with its larger equity base, reported Rs. 3.2 EPS, a growth of 22% YoY, which reflects steady improvement though lower in comparison.

Shree leads in EPS efficiency, UltraTech balances scale with return, while Ambuja continues steady shareholder value creation.

Conclusion

The Q1 FY26 results of UltraTech Cement, Ambuja Cements, and Shree Cement underline the strength of India’s cement sector. UltraTech reinforced its position as the largest and most diversified player with unmatched revenue and profit leadership. Ambuja stood out with record-breaking revenue and robust margin expansion, driven by operational efficiency and capacity integration. Shree Cement, despite being smaller in scale, delivered the highest percentage growth in profit and one of the strongest margins, showcasing disciplined execution.

Collectively, the performance highlights that each company brings unique strengths—UltraTech with scale, Ambuja with cost efficiency and growth, and Shree with profitability discipline—making the sector highly competitive and well-positioned for sustained growth.

For investors seeking smarter and seamless market opportunities, Enrich Money’s trading platform offers advanced tools, research insights, and a user-friendly experience. Discover a reliable way to grow your investments with Enrich Money.

Frequently Asked Questions

-

Which company reported the highest revenue in Q1 FY26?

Backed by acquisitions and strong volume gains, UltraTech Cement topped peers with revenue of ?21,275 crore.

-

Which cement company achieved the fastest profit growth?

Shree Cement delivered the strongest bottom-line performance, with profits nearly doubling at 95% YoY, even though its topline remained below that of UltraTech and Ambuja.

-

How did Ambuja Cements perform in Q1 FY26?

With capacity growth and disciplined cost management, Ambuja achieved a record revenue milestone of ?10,289 crore this quarter, reflecting 23% YoY growth.

-

Which company holds the largest market share in India’s cement industry?

UltraTech Cement dominates the market with its unmatched scale, supported by capacity expansions and acquisitions, making it the clear leader in terms of volumes and revenue.

-

What does the Q1 FY26 performance indicate for the cement sector?

The results highlight strong demand, efficiency improvements, and profitability across all three companies, showing the sector’s resilience and growth momentum in FY26.

Disclaimer: This blog is dedicated exclusively for educational purposes. Please note that the securities and investments mentioned here are provided for informative purposes only and should not be construed as recommendations. Kindly ensure thorough research prior to making any investment decisions. Participation in the securities market carries inherent risks, and it's important to carefully review all associated documents before committing to investments. Please be aware that the attainment of investment objectives is not guaranteed. It's important to note that the past performance of securities and instruments does not reliably predict future performance.